As humanoid robot makers move from demos to deployment, investors are backing the component that turns robots into working machines.

For the past two years, China’s embodied AI boom has centered on full humanoid platforms. In 2026, capital is moving down the stack. Dexterous hands, once treated as a lab component, are now being priced as a standalone supply-chain category.

The logic is practical. Walking robots attract attention, but hands create utility. A humanoid can only work in factories, warehouses, and service environments if it can grasp, sort, press, plug, assemble, and handle objects with control. That makes the hand layer commercially important and repeatable across multiple robot makers.

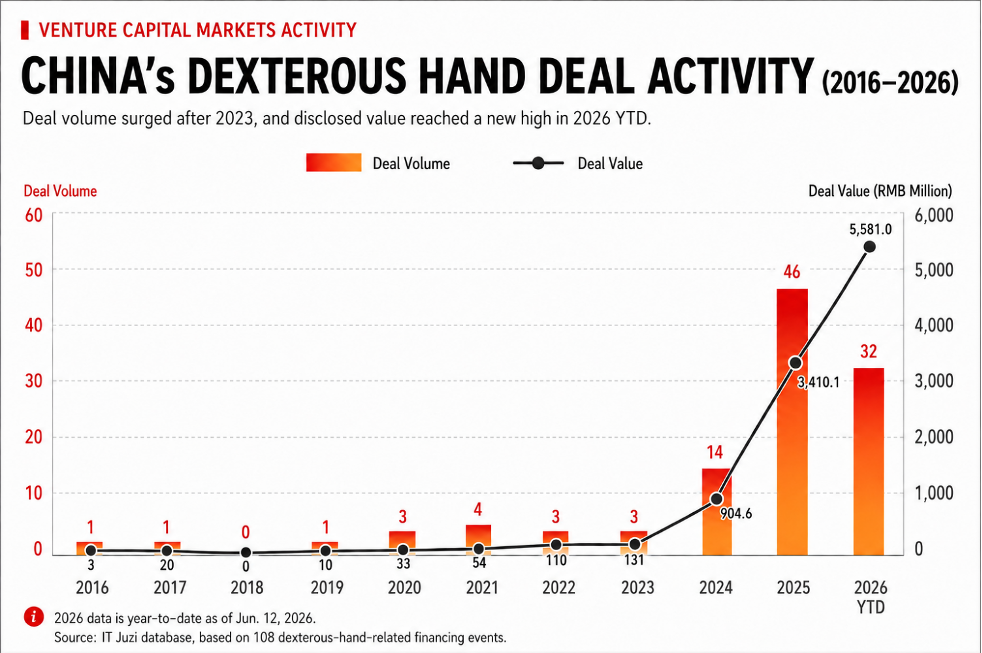

The 108 dexterous-hand-related funding rounds reveal a clear shift in investor attention:

- Before 2024, fundraising was sporadic, as dexterous hands remained a niche robotics component.

- From 2024, investment activity rose steadily alongside China’s embodied AI boom and the shift of humanoid robots from concepts to prototypes and pilot deployments.

- In 2025, the sector reached 46 funding rounds, with RMB 3.4 billion in disclosed investment.

- In the first half of 2026, it recorded 32 rounds and RMB 5.6 billion in disclosed investment, already exceeding the full-year total for 2025. Average round size rose 135%, from RMB 74 million to RMB 174 million.

Dexterous hands are moving from a research component to a strategic supply-chain category. Investors increasingly view them as critical infrastructure for deploying humanoid robots in factories, warehouses, and service environments.

Capital Signals Across the Dexterous Hand Market

This article highlights five companies that illustrate how capital is flowing into China’s dexterous hand market. Rather than forming a ranking, they represent distinct investment signals: valuation, production capacity, strategic investment, supply-chain positioning, OEM incubation, and early-stage pipeline formation.

The market is forming in three layers

China’s dexterous hand market is not moving in one straight line. Three layers are forming at the same time: valuation leaders, strategic component suppliers, and younger companies linked to future OEM demand.

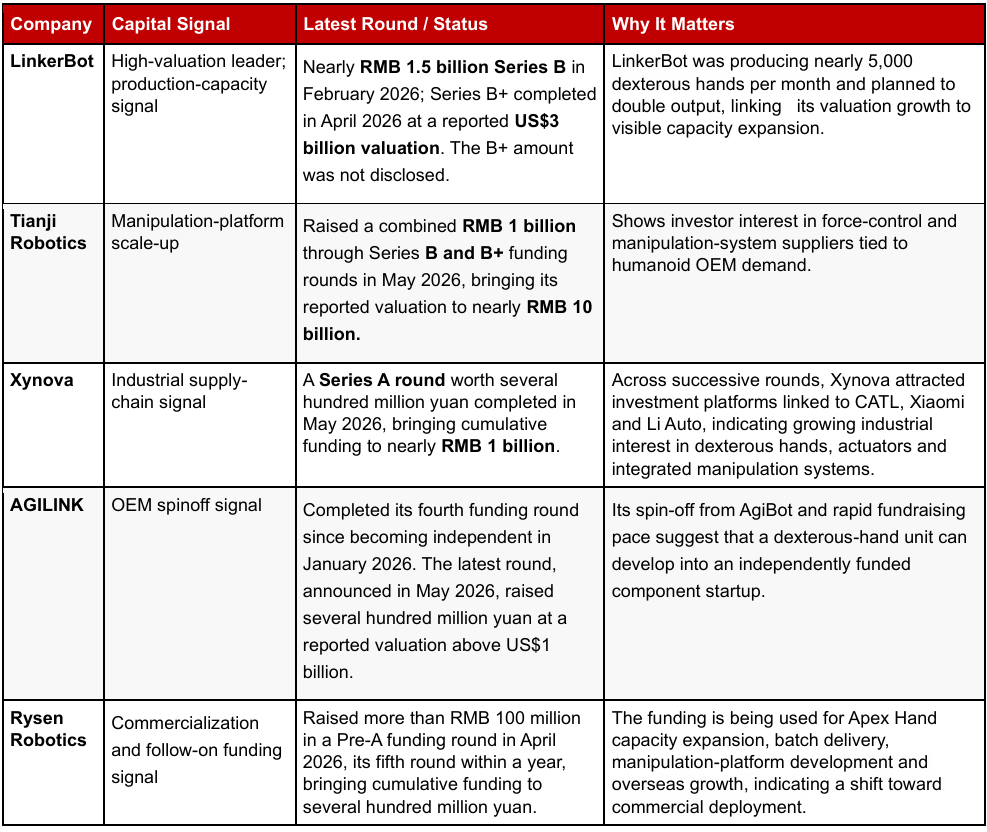

LinkerBot is the clearest valuation signal. Public reports indicate that the company completed a nearly RMB 1.5B Series B round, reached a RMB 10B post-Series B valuation, and later moved towards an even higher valuation after Series B+. The numbers still need publication-stage verification, but the direction is clear: investors are trying to identify default suppliers before large OEM procurement cycles fully accelerate.

This pricing is based on expectation, not only current revenue. If humanoid robot shipments scale, dexterous hands could become repeat-purchase hardware. Suppliers with stable performance, production capacity, and early OEM relationships may become hard to replace. This commercial potential is beginning to command a valuation premium from investors.

Strategic capital is treating the hand as a supply-chain asset

Tianji Robotics and Xynova show a different signal. They are not only raising money; they are attracting investors that care about the future structure of the robotics supply chain.

Tianji Robotics is reported to serve more than 45 humanoid robot OEM customers has with a backlog of more than 10,000 units. That customer base is a stronger signal than another demo video. It suggests that downstream demand has already started to form.

Xynova’s investor base points in the same direction. Investment platforms linked to CATL, Xiaomi, and Li Auto bring manufacturing experience, hardware supply-chain knowledge, and long-term exposure to intelligent machines. Their participation suggests that dexterous hands are being evaluated not only as a venture bet, but also as a potential control point in embodied AI hardware.

OEM spinoffs show the hand layer may become independent

AGILINK and Rysen Robotics should not be read through the same lens as LinkerBot. Their importance lies less in current valuation scale than in what they reveal about market structure.

AGILINK matters because it was incubated by AgiBot, one of China’s leading humanoid robot platforms. Its fourth funding round in five months shows that investors are willing to back dexterous-hand businesses as standalone component companies.

If a hand module can raise capital, sell to multiple customers, and build its own roadmap, it is no longer just an internal part of a robot stack. t is beginning to emerge as a standalone component category.

Rysen Robotics represents the commercialisation path. Proceeds from its latest funding round will be used to expand Apex Hand production capacity, support batch deliveries and develop overseas markets.

Investment Takeaways

The investment logic is shifting from platform hype to supply-chain pricing. Full humanoid robots still receive the most attention, but investors are now asking which component layers can capture durable value once OEMs begin to scale.

Dexterous hands are attractive because the revenue path may be shorter than full humanoid platforms. They are modular, upgradeable, and sellable across multiple robot makers. They may also enter industrial automation scenarios before full humanoid deployment becomes mature.

The market is still too early for a stable ranking. What matters is the role each company plays in the stack: leader, supplier, spinoff, or pipeline company.

Why It Matters

China’s humanoid robot race is no longer only about who can build the most impressive full-body machine. It is also about who controls the components that make the machine useful.

Dexterous hands sit at that intersection. They are technically difficult, commercially necessary, and increasingly investable. The companies attracting capital today are competing to become part of the default supply chain for embodied AI.

The next phase of China’s robotics market may therefore be less about demos and more about procurement. When OEMs begin to scale, the winners will not only be the robot brands on stage. They may also be the component suppliers hidden inside the machine.

Sources: IT Juzi database; Cyzone; 36Kr English; Gasgoo; Bloomberg; The Next Web; EqualOcean; Yicai Global; company announcements and public reporting reviewed by DayDayUp Research Team.

DayDayUp Research Team | Singapore & Beijing