Eight Companies, Billions of RMB, and What It Means for the World

Something shifted in China’s robotics industry in 2025 — and it happened faster than most observers expected.

Embodied AI, the field that combines large language models with physical robot bodies, moved from research labs and trade show floors into factories, warehouses, and commercial contracts. Capital followed at an unprecedented pace: Chinese embodied AI companies raised ¥73.5 billion ($10.8 billion) across 744 deals in 2025 alone. In the first five months of 2026, another ¥30 billion-plus entered the sector — averaging roughly ¥330 million per day.

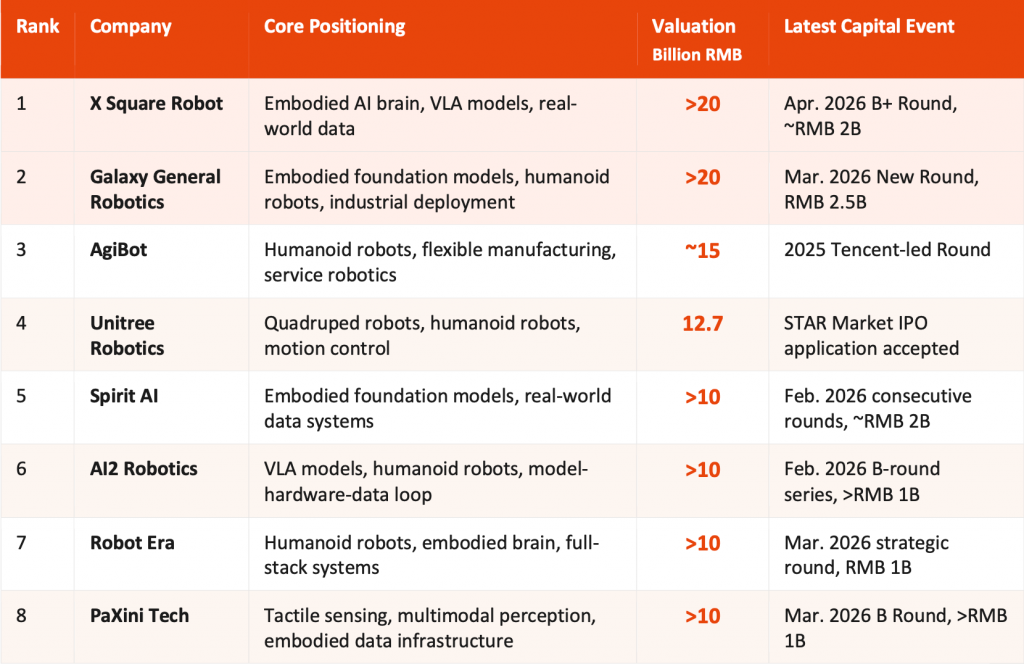

Eight companies have now crossed the RMB 10 billion valuation threshold. Two are valued above RMB 20 billion. The first IPO has been approved. A new industrial category is taking shape in real time.

This is no longer a story about China’s robotics ambitions. It is a story about a technology transition that is already underway — and one that will reshape manufacturing, logistics, and labour economics globally.

The Eight Companies Entering the Playoffs

China’s top eight embodied AI companies are not building the same thing. They are each competing to occupy — or control — a distinct layer of a technology stack that, in its mature form, will integrate AI foundation models, physical hardware, real-world training data, deployment infrastructure, and commercial go-to-market capacity. Understanding the stack is the prerequisite for understanding the race.

Embodied AI Brain: Galaxy General Robotics, Galaxea Dynamics, Spirit AI, and AI² Robotics

At the top of the stack are companies competing to build the intelligence layer of embodied AI.

Galaxy General Robotics, Galaxea Dynamics, Spirit AI, and AI² Robotics sit in this category.

Their strategic value is not limited to the robot body. It lies in the models, data systems, and intelligence infrastructure that allow robots to understand environments, interpret instructions, and execute physical tasks.

This is where vision-language-action systems become central.

A VLA system connects perception, language understanding, and physical execution. In simpler terms, it helps a robot understand what it sees, process what a human asks it to do, and decide what action to take next.

For overseas investors, this layer is particularly important because it looks less like traditional robotics manufacturing and more like AI infrastructure applied to the physical world.

Robot bodies may be replaced, upgraded, or produced by different hardware vendors. But a generalisable intelligence layer that can run across different platforms, task types, and deployment environments could become much more valuable.

In the long run, the “brain layer” may become the operating system of physical AI.

The key investment question is therefore not simply whether these companies can build advanced models.

It is whether their models can generalise, improve through real-world data, and translate intelligence into reliable physical action.

Robot Body: Unitree Robotics, AgiBot, and Robot Erae Robotics and AgiBot

The second layer is where embodied AI becomes visible to customers.

This is the layer of robot bodies, full-stack systems, motion control, hardware integration, supply chain execution, and commercial deployment.

Unitree Robotics, AgiBot, and Robot Era are positioned here.

Unitree Robotics is one of the most important companies to watch because it represents commercial discipline in a sector that is still highly experimental. The company has built strong global recognition through quadruped robots and is now moving further into humanoid systems. Its relevance is not only technological. It also reflects China’s strength in hardware iteration, cost control, and productisation.

AgiBot represents another important route. It is one of China’s most visible humanoid robotics companies, backed by strong technical narratives and strategic capital. The market expectation is clear: AgiBot needs to convert visibility into deployment volume, customer traction, and recurring commercial value.

Robot Era adds another dimension to this layer. Its relevance lies in connecting robot systems with industrial scenarios. In embodied AI, commercialisation is not just about building a robot that can move. It is about integrating robots into factories, warehouses, logistics workflows, and other operational environments where ROI can be measured.

This layer is difficult because it requires multiple capabilities at once.

A company needs hardware engineering, motion control, supply chain management, safety systems, software integration, field operations, and after-sales support. A robot that performs well in a controlled demo environment is very different from a robot that can operate repeatedly in a real commercial setting.

For investors, the core question is straightforward:

Can these companies build robots that work reliably, repeatedly, and economically in the real world?

If the answer is yes, they are no longer just robotics startups.

They become automation infrastructure companies.

Perception Infrastructure: PaXini Tech

The third layer is perception infrastructure.

PaXini Tech focuses on tactile sensing and multimodal perception, a critical but often under-discussed part of embodied AI.

For robots to operate in the physical world, vision is not enough. They also need to understand pressure, force, contact, and material interaction. This becomes especially important in tasks that require grasping, handling, assembling, or manipulating objects with precision.

From an investment perspective, PaXini Tech represents a focused infrastructure bet.

As robot bodies become increasingly standardised, specialised sensing capabilities may become an important source of differentiation. In that sense, PaXini is not simply a component company. It is addressing one of the key bottlenecks that will determine whether embodied AI can move from controlled demos to real-world work.

What Makes This Different from Previous Robotics Cycles?

China has invested in robotics before. Previous waves produced capable hardware in controlled environments but limited commercial adoption. The current cycle is different in four important ways.

Foundation models have changed what robots can do. The rapid improvement of large language models from 2022 onwards created, almost as a byproduct, the architectural foundation for vision-language-action systems. The ability to train robots on language instructions, visual inputs, and physical feedback simultaneously — and to generalise that training across task types and environments — compressed the timeline for commercially useful embodied AI from “decades away” to “under active deployment.” Companies that began serious research in 2022 or 2023 are running real pilots with real customers as of mid-2026.

Data loops are becoming the primary competitive moat. In previous robotics cycles, success was measured in lab performance metrics and trade show demonstrations. This cycle will be decided by data. Every hour a robot operates in a factory, warehouse, or logistics hub generates training signal that refines the models running all subsequent robots. Companies that achieve early deployment at scale compound a model advantage in ways that late entrants cannot replicate. This is the structural insight most coverage of Chinese robotics misses: the robot body is a distribution mechanism. The real product is the deployment data.

Real-world deployment — not demos — is the benchmark. Commercial contracts, production unit counts, and disclosed unit economics are now the metrics that matter. Unitree’s IPO application forces a public reckoning with what this sector is actually worth. Every other valuation in the cohort will ultimately be measured against what the public market decides Unitree is worth.

China’s manufacturing ecosystem provides structural cost advantages that are compounding. China’s precision electronics supply chain — motors, sensors, actuators, and structural components — is not merely cost-competitive; it is qualitatively superior in iteration velocity. A Chinese robotics startup can test, redesign, and remanufacture a motor assembly in weeks. This is the product of decades of sustained manufacturing investment, and it is why the cost curve is falling faster than most observers anticipated. IDTechEx projects average humanoid robot prices declining 68% by 2030 — from roughly $115,000 in 2024 to around $37,000. Goldman Sachs forecasts manufacturing costs reaching $15,000–$20,000 per unit at scale. Bank of America’s research projects commercial-grade units at $13,000–$17,000 by the same year. Unitree’s G1 already retails at $16,000 today.

Why Global Companies Should Pay Attention

The embodied AI transition carries structural implications for global manufacturers, supply chains, and labour markets — and the timeline is compressing faster than most corporate planning assumptions reflect.

The productivity impact is real, and deployment has already begun. Figure AI’s F.02 humanoid contributed to the production of more than 30,000 BMW vehicles at the Spartanburg plant in the United States. BMW announced its first European humanoid robot deployment at its Leipzig facility in February 2026. These are not pilots in controlled conditions; they are production-line deployments generating commercial output. For global manufacturers, the question is no longer whether embodied AI will reach commercial maturity — it is whether their organisations are prepared to evaluate and adopt it on a competitive timeline.

Supply chain implications are strategic, not just operational. Companies that depend on labour-intensive manufacturing in any geography need a forward view on how embodied AI changes their cost structures. As unit prices move toward the $20,000–$30,000 range projected by 2030, the economics of robot adoption become compelling in an expanding set of manufacturing environments. Procurement leaders and operations teams that begin evaluation now will have a meaningful advantage over those waiting for the technology to “fully mature.”

The standards race is underway. Whoever achieves early large-scale deployment sets the de facto performance benchmarks, data protocols, safety standards, and integration interfaces that subsequent adopters build around. In enterprise software, this is the standards lock-in dynamic. In physical AI, it will operate similarly — but intersecting with regulatory frameworks, workplace safety law, and national industrial policy in ways that software standards do not. Companies that achieve first-mover deployment will have significant influence over how global standards evolve.

What It Means for Southeast Asia

Southeast Asia occupies a specific position in the global embodied AI deployment sequence — one that requires both strategic realism and forward planning.

The first wave of large-scale commercial deployment is concentrating in high-labour-cost markets. Japan Airlines’ Unitree G1 trials at Haneda Airport, BMW’s humanoid deployments in the United States and Germany, and early logistics automation in South Korea all follow the same economic logic: where labour is expensive and hard to source, the payback economics of a $50,000–$100,000 robot are compelling today. Southeast Asia, with structurally lower labour costs, is more realistically positioned as a second-wave market — one that becomes commercially compelling as robot unit prices fall toward the $20,000–$30,000 range projected by 2030.

Manufacturing and warehousing are the most immediate verticals to watch. Southeast Asian factories in electronics, consumer goods, and automotive components represent the sector where cost curves will intersect with adoption thresholds earliest. Logistics and warehousing operations — particularly those serving the region’s fast-growing e-commerce sector — are a natural early deployment environment as unit prices decline and deployment tooling matures.

Singapore’s strategic role is as a hub, not just a market. The more immediate opportunity for Singapore-based investors, corporates, and professional services firms is not as end-market adopters of embodied AI hardware, but as the governance, financing, and IP structuring layer connecting Chinese technology supply with global demand. Companies building Singapore-domiciled holding structures, neutral IP jurisdictions, and transparent international governance frameworks will access a significantly wider global customer base. This is an underpriced source of competitive advantage — and one where Singapore has genuine structural advantages to offer.

Industrial services and supply chain transformation will follow. As embodied AI platforms mature beyond initial manufacturing applications, industrial services, inspection, maintenance, and logistics will represent the next adoption frontier in Southeast Asia. Companies managing cross-border supply chains that currently depend on labour-intensive processes should begin scenario planning that incorporates this transition now.

Conclusion

The winners of China’s embodied AI race will not necessarily build the most impressive robots.

They will build the strongest data loops — accumulating operational intelligence from real-world deployment at scale. They will build the deepest deployment networks — reaching factories, warehouses, and service environments across China and increasingly beyond. And they will build the clearest commercial discipline: unit economics that hold, governance structures that travel, and revenue models that compound.

Eight companies are in the playoffs. The next eighteen months will determine who advances — and what the rest of the world has left to work with.

DayDayUp Research Team | Singapore & Beijing

Sources:

Brookings Institution — China’s Shrinking Population and Constraints on Its Future Power

World Economic Forum — Future of Jobs Report 2025

MERICS — Embodied AI: China’s Ambitious Path (April 2026)

IDTechEx — Humanoid Robot Price Falls 68% by 2030, Six-Month Payback Possible Now

Goldman Sachs — The Global Market for Humanoid Robots Could Reach $38 Billion by 2035

Bank of America Robotics Research (via There’s a Robot for That) — Humanoid Robot Cost 2026

Figure AI — F.02 Contributed to the Production of 30,000 Cars at BMW

BMW Group Press — BMW Group to Deploy Humanoid Robots in Production in Germany for the First Time